Understanding the US Tax System: A Simple Guide for Every American

Every year, millions of Americans dread tax season. The forms are confusing, the rules seem to change constantly, and one wrong move feels like it could trigger an audit. But here's the truth: the US tax system, while complex, follows a logical structure that anyone can understand with the right explanation. This guide breaks it all down — from how income tax brackets actually work to the deductions and credits that could save you thousands.

How the US Federal Income Tax Works

The United States uses a progressive tax system, which means the more you earn, the higher the tax rate — but only on the portion of income that falls within each bracket. This is a point of confusion for many Americans.

If you're in the 22% tax bracket, you do not pay 22% on your entire income. You pay 10% on the first portion, 12% on the next, and 22% only on the income that falls within that range.

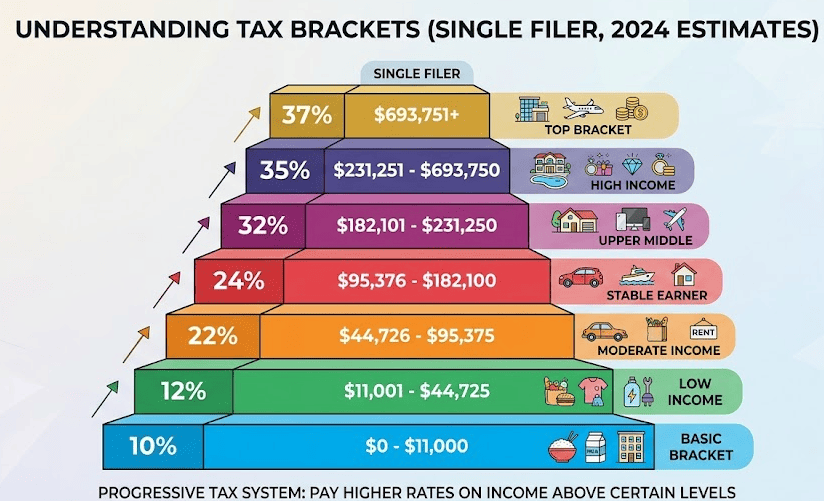

For 2025, the federal income tax brackets for single filers are:

- 10% on income up to $11,925

- 12% on income from $11,926 to $48,475

- 22% on income from $48,476 to $103,350

- 24% on income from $103,351 to $197,300

- 32%, 35%, and 37% on higher income levels

Understanding this prevents the common fear that "a raise will put me in a higher bracket and I'll take home less." That is mathematically impossible under a progressive system.

Federal vs. State vs. Local Taxes

Federal income tax is just one layer. Depending on where you live, you may also owe:

State income tax — Most states levy their own income tax, ranging from under 3% (North Dakota) to over 13% (California). Seven states — including Florida, Texas, and Nevada — have no state income tax at all, which is a significant factor for many Americans when choosing where to live.

Local taxes — Some cities (New York City, Philadelphia, Detroit) impose their own local income taxes on top of state and federal.

FICA taxes — These fund Social Security (6.2%) and Medicare (1.45%), and are automatically withheld from every paycheck. Your employer matches these amounts.

Sales tax — Unlike VAT systems in Europe, the US sales tax is applied at point of purchase and varies by state and even county, ranging from 0% to over 10%.

Standard Deduction vs. Itemizing

Every American taxpayer gets to reduce their taxable income through deductions. You choose one of two paths:

Standard deduction — For 2025, this is $15,000 for single filers and $30,000 for married couples filing jointly. You claim this flat amount with no documentation needed. The majority of Americans take this route.

Itemized deductions — If your qualifying expenses exceed the standard deduction, you can itemize. Common itemized deductions include mortgage interest, state and local taxes (SALT, capped at $10,000), charitable contributions, and significant medical expenses.

For most Americans — especially renters and those with simpler financial lives — the standard deduction is the better choice and simplifies filing considerably.

Tax Credits: Better Than Deductions

While deductions reduce your taxable income, tax credits directly reduce your tax bill dollar for dollar — making them far more valuable.

Key federal tax credits to know:

Earned Income Tax Credit (EITC) — Designed for low-to-moderate income workers, this credit can be worth up to $7,830 depending on income and number of children. One of the most impactful credits available.

Child Tax Credit — Up to $2,000 per qualifying child under 17, with up to $1,700 refundable.

American Opportunity Credit — Up to $2,500 per year for the first four years of higher education expenses.

Retirement Savings Contributions Credit (Saver's Credit) — Up to $1,000 ($2,000 for couples) for contributions to a 401(k) or IRA, specifically for lower-income earners.

Energy Efficiency Credits — Credits for installing solar panels, energy-efficient windows, or purchasing an electric vehicle (subject to income and vehicle eligibility limits).

How to File Your Taxes

Most Americans file their taxes between January and April 15th each year. You have several options:

Free File — If your income is below $84,000, the IRS Free File program offers free federal tax preparation software through partner companies at irs.gov.

Tax software — TurboTax, H&R Block, and TaxAct are the most widely used paid platforms. They guide you through every step with interview-style questions.

Tax professional — For complex situations — self-employment, rental income, significant investments, or major life changes — a CPA or enrolled agent is worth the cost.

Important: If you can't file by April 15th, you can request an automatic six-month extension. The extension gives you more time to file — not more time to pay any taxes owed.

One Tip That Could Save You Thousands

If your employer offers a Health Savings Account (HSA) or Flexible Spending Account (FSA), maximize your contributions. HSA contributions are triple tax-advantaged: tax-deductible going in, tax-free growth, and tax-free withdrawals for medical expenses. For 2025, individuals can contribute up to $4,300 to an HSA.

Tax planning isn't just for April. The best tax strategy is one built throughout the year — adjusting withholdings, maximizing retirement contributions, and timing major financial decisions with your tax situation in mind.