The Future of Personal Finance in America: Smart Strategies for Building Wealth in 2026

Managing money has never been more important—or more challenging—than it is today. Rising living costs, evolving investment opportunities, advancements in financial technology, and economic uncertainty have changed how Americans think about their finances. Whether you're just starting your financial journey or looking to optimize an established portfolio, understanding modern personal finance strategies can help you achieve long-term financial security.

In this guide, we'll explore the most important trends shaping personal finance in the United States and provide practical tips to help you make smarter financial decisions in 2026 and beyond.

Why Financial Literacy Matters More Than Ever

Financial literacy is no longer a luxury; it's a necessity. Americans today have access to more financial products and services than ever before, from digital banking apps to cryptocurrency investments and AI-powered financial advisors.

However, with more options comes greater responsibility. Poor financial decisions can have long-lasting consequences, including excessive debt, insufficient retirement savings, and missed investment opportunities.

Key areas every American should understand include:

- Budgeting and cash flow management

- Credit scores and debt management

- Emergency savings

- Investing fundamentals

- Retirement planning

- Tax optimization

- Insurance protection

Developing financial literacy empowers individuals to make informed decisions and avoid common financial pitfalls.

The Importance of Creating a Realistic Budget

A budget is the foundation of financial success. Contrary to popular belief, budgeting doesn't restrict spending—it provides clarity and control.

Many financial experts recommend the 50/30/20 rule:

- 50% for necessities (housing, transportation, groceries)

- 30% for discretionary spending

- 20% for savings and debt repayment

While this framework may not fit everyone perfectly, it offers a useful starting point.

Modern budgeting apps can automatically categorize expenses, track spending habits, and identify areas where money may be leaking unnoticed.

Common Budgeting Mistakes

- Ignoring irregular expenses

- Underestimating discretionary spending

- Failing to track subscriptions

- Not adjusting for inflation

- Neglecting emergency savings

The most successful budgets are flexible and reviewed regularly.

Building an Emergency Fund

Unexpected events can disrupt even the most carefully planned finances. Job loss, medical emergencies, vehicle repairs, and home maintenance costs can quickly create financial stress.

Financial planners generally recommend maintaining an emergency fund that covers:

- 3–6 months of essential living expenses

- Higher reserves for self-employed individuals

- Additional savings for households with variable income

A high-yield savings account can provide both liquidity and modest interest earnings.

Benefits of an Emergency Fund

- Reduces reliance on credit cards

- Prevents long-term debt accumulation

- Provides peace of mind

- Creates financial flexibility during economic downturns

Even saving a small amount consistently can lead to substantial protection over time.

Understanding Credit and Debt Management

Credit remains one of the most important financial tools available to Americans. A strong credit profile can significantly impact:

- Mortgage approval

- Auto loan rates

- Insurance premiums

- Rental applications

- Employment opportunities in certain industries

Ways to Improve Your Credit Score

- Pay bills on time

- Keep credit utilization below 30%

- Avoid unnecessary hard inquiries

- Maintain older accounts

- Monitor credit reports regularly

At the same time, consumers should prioritize eliminating high-interest debt, particularly credit card balances that can carry annual percentage rates exceeding 20%.

Debt Reduction Strategies

Snowball Method

Pay off the smallest debts first while maintaining minimum payments on larger balances.

Advantages:

- Builds motivation quickly

- Creates psychological momentum

Avalanche Method

Focus on debts with the highest interest rates first.

Advantages:

- Minimizes total interest paid

- Faster path to becoming debt-free

Both methods can be effective depending on personal preferences and financial circumstances.

Investing for Long-Term Wealth Creation

Investing remains one of the most powerful ways to build wealth over time. While market volatility can be intimidating, history has shown that disciplined long-term investing often outperforms attempts to time the market.

Popular Investment Options

Stocks

Offer potential for high returns but carry higher risk.

Bonds

Typically provide stability and predictable income.

Index Funds

Allow investors to gain diversified exposure to large segments of the market at low cost.

Exchange-Traded Funds (ETFs)

Provide flexibility and diversification with lower fees than many actively managed funds.

Real Estate

Can generate both appreciation and passive income.

Many financial advisors encourage diversification across multiple asset classes to reduce overall portfolio risk.

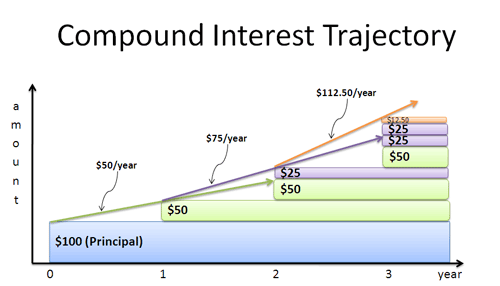

The Power of Compound Growth

One of the most important concepts in investing is compound interest.

genui{"finance_economics_learning_block":{"type_id":"COMPOUND_INTEREST","content":"FV = PV(1+r)^n"}}

The earlier an individual starts investing, the more time their money has to compound and grow.

For example:

- Investing $500 per month at age 25

- Earning an average annual return of 8%

- Continuing until age 65

Can potentially result in a portfolio worth over $1.7 million.

Time is often a more powerful factor than investment amount.

Retirement Planning in a Changing Economy

Retirement planning has evolved significantly over the past few decades.

Traditional pensions have become less common, placing greater responsibility on individuals to fund their retirement.

Popular Retirement Accounts

401(k)

Employer-sponsored retirement plan that often includes matching contributions.

Traditional IRA

Tax-deferred retirement account.

Roth IRA

Contributions are made with after-tax dollars, but qualified withdrawals are tax-free.

Maximizing Retirement Savings

- Contribute enough to receive full employer matching

- Increase contributions annually

- Rebalance investments periodically

- Avoid early withdrawals

Retirement planning should be viewed as a lifelong process rather than a one-time event.

Financial Technology Is Transforming Money Management

Technology continues to reshape personal finance.

Today's consumers can access sophisticated financial tools directly from their smartphones.

Popular fintech innovations include:

- Digital banking

- Robo-advisors

- Peer-to-peer payments

- Automated investing

- AI-powered budgeting tools

- Real-time fraud monitoring

These tools can help individuals automate financial decisions and improve consistency.

Benefits of Automation

Automating savings and investments helps remove emotional decision-making and creates disciplined financial habits.

Examples include:

- Automatic retirement contributions

- Recurring investment purchases

- Automated bill payments

- Scheduled savings transfers

Automation often leads to higher long-term savings rates.

Protecting Your Finances From Inflation

Inflation remains one of the biggest challenges facing consumers.

Even moderate inflation can significantly reduce purchasing power over time.

For example, an item costing $100 today may cost considerably more within a decade.

Strategies to Combat Inflation

- Increase income through skill development

- Invest in growth-oriented assets

- Maintain diversified portfolios

- Avoid excessive cash holdings

- Review spending regularly

Long-term investors often focus on assets that historically outpace inflation, such as stocks and real estate.

The Rise of Side Hustles and Multiple Income Streams

Many Americans are no longer relying solely on a single source of income.

The growth of digital platforms has created opportunities for:

- Freelancing

- Consulting

- Content creation

- Online businesses

- E-commerce

- Digital product sales

Multiple income streams can improve financial resilience and accelerate wealth-building goals.

Benefits of Additional Income

- Faster debt repayment

- Increased investment contributions

- Enhanced financial security

- Greater career flexibility

Even a modest side income can have a significant long-term impact when invested consistently.

Financial Planning for Families

Families face unique financial challenges, including childcare costs, education expenses, healthcare needs, and long-term planning responsibilities.

Important family financial goals may include:

- College savings

- Homeownership

- Insurance coverage

- Estate planning

- Retirement security

Regular financial discussions help ensure all household members remain aligned with shared goals.

Essential Types of Insurance

- Health insurance

- Auto insurance

- Homeowners insurance

- Disability insurance

- Life insurance

Insurance serves as a critical layer of financial protection against unforeseen events.

Final Thoughts

Financial success is rarely the result of a single decision. Instead, it comes from consistent habits practiced over many years. Building a budget, maintaining an emergency fund, managing debt responsibly, investing regularly, and planning for retirement are foundational steps toward long-term financial stability.

As financial technology continues to evolve and economic conditions change, Americans who prioritize financial literacy and disciplined money management will be best positioned to achieve their goals.

The future of personal finance belongs to individuals who take proactive control of their financial lives today. Whether you're saving your first thousand dollars, investing for retirement, or building generational wealth, every smart financial decision moves you one step closer to lasting financial freedom.