Navigating the 2026 Mid-Year Shift: Interest Rates, Market Fragility, and Your Money

The U.S. economy in 2026 is acting like a twin-engine plane where one engine is roaring at full throttle while the other is sputtering.

On one side, we are witnessing a massive productivity boom fueled by the accelerating corporate deployment of artificial intelligence. On the other hand, everyday consumers are facing persistent, sticky inflation hovering around 3% to 3.4%, an unsettled labor market, and a housing landscape that has pricing dynamics completely locked in place.

For the average investor or household trying to navigate their personal finances, the traditional playbooks no longer apply. We are moving into the second half of 2026 facing a highly volatile macroeconomic environment.

Whether you are looking to buy a home, adjust your retirement portfolio, or figure out where to park your cash, here is the ground-truth breakdown of what is happening in U.S. finance right now—and how you can adapt.

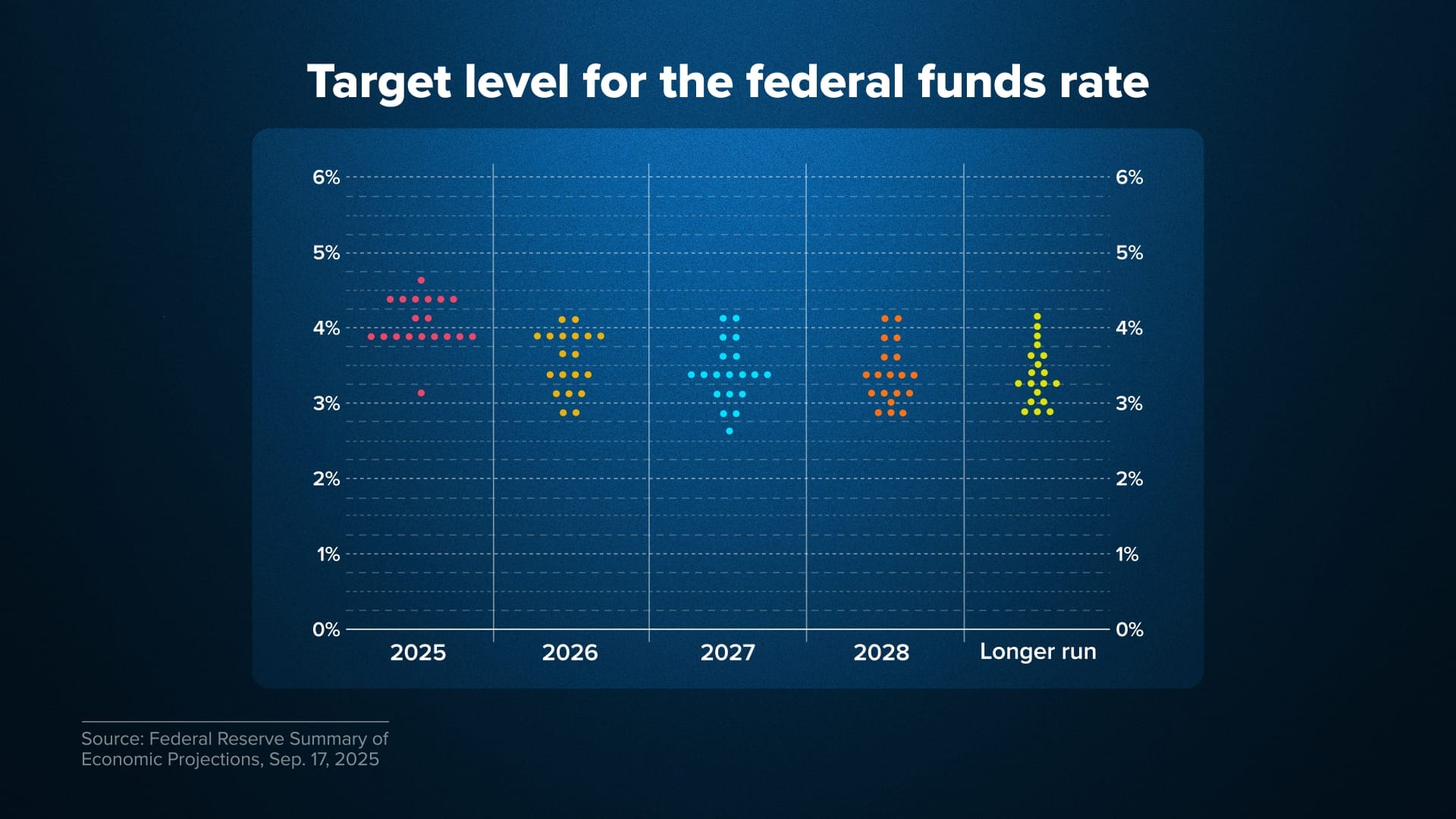

1. The Federal Reserve's Balancing Act: The Path to Neutral

For the last several quarters, the market's obsession has been entirely centered on the Federal Reserve and its new leadership under Chairman Kevin Warsh. The narrative has shifted from aggressively hiking rates to trying to find the "neutral rate"—the sweet spot where monetary policy neither stimulates nor restricts economic growth.

As we move through mid-2026, the Effective Federal Funds Rate rests around 3.87%, with the Secured Overnight Financing Rate (SOFR) hovering just above 4%. The consensus among institutional researchers, including baseline data from RSM and J.P. Morgan, points toward a gradual, cautious glide path. The Fed is widely projected to target a policy range between 3.0% and 3.25% by the end of the year.

However, this isn't a guaranteed victory lap. The domestic labor market has entered a distinct "low-hire, low-fire" phase. The unemployment rate has nudged up to 4.3%, signaling that while massive corporate layoffs aren't happening, finding a new job is taking considerably longer. Because wage growth has cooled to around 3.6%, the Fed has the justification it needs to ease rates, even if the Consumer Price Index (CPI) refuses to drop down to that elusive 2% target.

What This Means for Your Cash:

Holding massive amounts of money in standard cash or short-term vehicles worked wonders when yields were at their peak. However, as the Fed continues its gradual trimming, pure cash allocations are increasingly acting as a drag on wealth. When you factor in sticky 3% inflation, the real purchasing power of idle cash is actively eroding. If you have been sitting on the sidelines in a High-Yield Savings Account (HYSA), it is time to look at locking in yields through intermediate-term bonds or shifting capital back into equities and real assets.

2. The 2026 Housing Market: Stalling at Zero

If you've been waiting for a dramatic, 2008-style crash in U.S. real estate to finally buy a home, the data for 2026 brings a cold dose of reality. Nationally, house prices aren't crashing—they are simply flatlining.

According to major real estate indexes and J.P. Morgan Research, national home price growth is projected to stall at exactly 0% for the remainder of 2026. The extreme price growth of the early 2020s has finally burned out, but structural gridlock remains.

| Housing Metric (Mid-2026) | Current Status | Impact on Buyers |

| 30-Year Fixed Mortgage | Hovering between 6.0% and 6.5% | Keeps monthly payments historically high |

| National Price Growth | Stalled near 0% year-over-year | Halts aggressive bidding wars but preserves baseline high costs |

| Unsold Inventory | Rising slowly (~4.4 months of supply) | Gives buyers slightly more room to negotiate inspection concessions |

The housing market is highly regionalized right now. In areas across the West Coast and parts of the Sun Belt—which saw a massive pandemic-era construction boom—a sudden glut of new inventory is forcing prices slightly downward. Conversely, the Northeast and Midwest remain highly constrained by low supply, keeping prices stubborn.

To keep inventory moving, homebuilders have turned heavily toward financing incentives rather than cutting sticker prices. If you look at new construction today, developers are routinely offering aggressive mortgage rate buydowns (often buying the buyer's rate down into the 5% range for the first few years) to clear their books.

The Strategic Move:

If you are a prospective buyer, the current market gives you leverage that didn't exist two years ago. Homes are sitting on the market longer, meaning you can successfully negotiate for seller concessions, repairs, or rate buydowns. Avoid stretching your budget to the absolute limit; instead, focus heavily on the monthly payment math, knowing that refinancing opportunities may materialize if the Fed hits its 3% target by 2027.

3. Stock Market Bifurcation: The AI Supercycle vs. Valuation Fears

Wall Street in 2026 is defined by extreme concentration. The dominant narrative driving corporate earnings remains the second and third innings of the Artificial Intelligence enterprise rollout. We have moved past the initial phase of pure speculation; companies are now actively integrating these technologies to generate measurable productivity gains and margin expansions.

This tech-driven productivity tailwind is the primary reason why broader U.S. GDP growth is projected to hit a healthy 2.2% this year. However, it has created a massive valuation gap between the mega-cap tech sector and the rest of the market.

Many value-focused investors are growing anxious that the S&P 500 is trading at stretched historical multiples, leaving very little margin for error. Furthermore, external risks are lingering on the periphery:

- Global Fragmentation & Tariffs: Ongoing trade protectionism and shifting supply chains are keeping structural costs higher for manufacturing firms.

- Geopolitical Volatility: Energy infrastructure and international trade routes remain under pressure, making sudden commodity shocks a constant threat.

- The Fiscal Deficit: The U.S. federal budget deficit is projected to hit a staggering $1.9 trillion in fiscal year 2026, pushing public debt to 101% of GDP. This massive fiscal expansion keeps the broader economy warm but threatens to keep long-term Treasury yields elevated.

Portfolio Readjustment:

A traditional, static portfolio split evenly between stocks and bonds is facing distinct pressures due to the positive correlation between equity volatility and sticky inflation. Wall Street's top wealth managers are increasingly urging investors to diversify into alternative strategies, defensive sectors (like aerospace, infrastructure, and defense), and real assets like gold or commodities that offer a structural hedge against rolling inflationary shocks.

4. The Consumer's Dilemma: Finding Yield in a Cooling Economy

For everyday Americans, personal finance in the latter half of 2026 is an exercise in defensive budgeting. While the macroeconomic headlines talk about a "soft landing," consumer sentiment remains deeply sensitive to everyday pocketbook pressures. Electricity, insurance premiums, and healthcare costs are consuming a larger percentage of the average household's net operating income than they did a decade ago.

With the labor market loosening up, workers no longer have the immense wage-leverage they possessed during the post-pandemic hiring boom. The strategy must pivot from aggressive income jumping to optimized capital preservation.

3 Personal Finance Rules for the Remainder of 2026:

- Lock in Fixed Fixed-Income Yields Now: If you have capital sitting in cash, look to lock in mid-term yields through Certificates of Deposit (CDs) or multi-year Treasury notes before the Federal Reserve cuts rates down into the low 3% range.

- Audit Debt Structures: If you are holding any variable-rate debt—such as credit card balances or personal lines of credit—prioritize paying them off immediately. While the Fed is easing, interest rates are still structurally higher than the ultra-cheap era of the 2010s.

- Focus on Quality Assets: Whether you are buying equities or real estate, prioritize entities with fortress balance sheets. In a "stagflation-lite" environment where growth is moderate but costs stay high, companies with high pricing power and low debt loads will consistently outperform.

Summary: Staying Agile in an Unsettled Era

The theme of U.S. finance in 2026 is calculated patience. The wild swings of the early 2020s are giving way to an economy that is grinding along under the weight of higher structural costs, massive national debt, and transformative tech innovations.

By understanding that inflation has a structurally higher floor, that the housing market has entered a period of price stabilization, and that the Fed is hunting for a neutral baseline, you can position your personal balance sheet to weather the volatility. Focus on locking in yields, negotiating housing concessions, and ensuring your investment portfolio has a healthy mix of tech-driven growth and real-asset protection.